GSTZen is a User-friendly solution with Committed Support by their Professional staff. I appreciate their proactive approach for improvements as and when required by Businesses and Compliances.

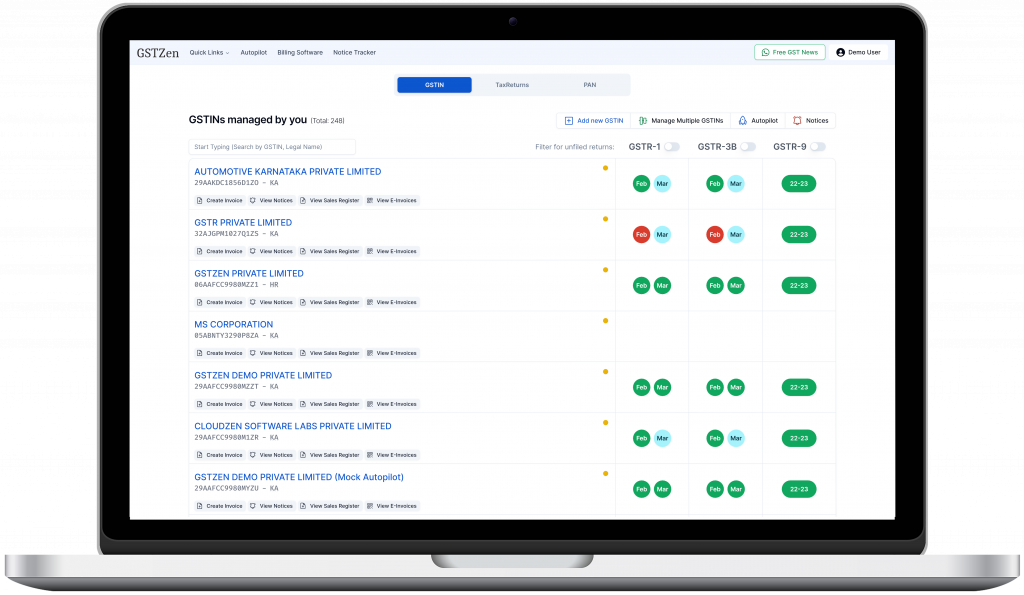

File GST Returns

Catch Errors Early & File Returns On-Time, Every time!

Data Validation

Gone are the days of errors in your GST returns!

Hundreds of data validation & check points to avoid manual errors.

Data Auto-population

Auto-populated annual return based on values from your monthly returns.

Only verify, update if needed and your return will be filed before you know it.

GSTR 1 Filing in 8 mins

Filing GSTR 1 after e-Invoice introduction made easier in GSTZen.

Download auto-populated e-Invoice details and reconcile with books before filing return through GSTZen.

GST and E-Way Bill Reports

GST and e-Way bill reports on the click of a button

Want to follow and ensure that your suppliers are filing their returns? GSTZen's Vendor filing status report provides filing details of your suppliers and customers in a handy Excel Report.